- The Broken Deal Newsletter

- Posts

- How to blow up a deal by mixing EBITDA Multiples AND Asset Values (1)

How to blow up a deal by mixing EBITDA Multiples AND Asset Values (1)

Issue 2 of the Broken Deal Newsletter

Matt Duckworth & Patrick Thornton

October 06, 2024

THIS WEEK IN BROKEN DEALS

Welcome to the Broken Deal Newsletter!

Here’s what’s in store for this week:

Announcement: Let’s meet up at McGuire Woods in Dallas Oct 15-16th

Best Link: A true war story on why you need to talk to your lending partners before you submit an LOI

The Graveyard: A business owner’s worst nightmare comes true when he prices his business using a multiple of EBITDA AND get extra credit for inventory and A/R.

Work With Us: We just opened up a new program for small growing M&A Advisors and Brokers to get Wall Street level quality analyst help with their deals on a success-fee basis. Book a call with us below to learn more.

ANNOUNCEMENT

October is upon us and it’s that time of the year again…

No, it’s not the Catalina Wine Mixer.

I’m talking about the McGuire Woods Independent Sponsor Private Equity Conference on October 15-16th.

If you’re going to be in Dallas during the conference, let us know. Patrick will be there meeting with our contacts in family offices, private equity and lenders. We’re actively looking to build relationships with industry people who have a focus in lower middle market industrial / manufacturing.

If that’s you, shoot us a note at matt at rhapsodi.net. We’d love to connect.

BEST LINKS

Matt’s Favorites

Finance & Capital

Salability

THE GRAVEYARD

You don’t get an EBITDA Multiple AND Asset Value at the same time.

About a year ago, I found myself reaching out to a broker regarding a manufacturing business. The usual exchange followed: financials, asking price, and the inevitable call to discuss how much it was really worth.

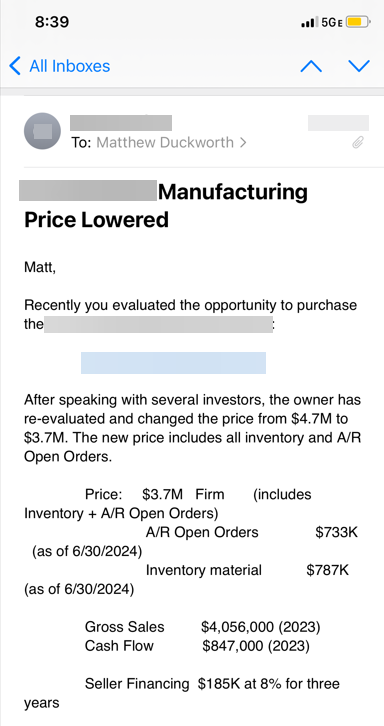

The seller’s business was doing $800k in EBITDA—a number that sounds terribly important and impressive, even though it mostly means “how much money before we remember to subtract everything else.” Then the broker (Lets call him John) revealed the asking price: $4.7 million, with an extra $1 million tacked on for inventory and accounts receivable, bringing the grand total to $5.7 million.

I paused. “John,” I said, as if explaining to someone that the sky is, in fact, blue, “Let me get this straight—you’re asking $5.7 million for a business making $800k a year. That’s more than seven times EBITDA. Isn’t that, well, rather high?”

John, with the air of someone caught in the act of selling a bridge, admitted that it was negotiable. The seller had priced it that way to pay off his debt and get paid for his inventory. In short, his retirement plan was my problem.

Naturally, I passed on the deal, hoping to leave it behind like an inconveniently timed phone call from an overly chatty relative. But a few months later, the broker called, practically begging me to reconsider, now claiming that the new price “includes inventory and A/R”.

By this time I was already in the throes of another transaction and passed (again). It was terrible to see.

Why?

Because here was a perfectly salable business with perfectly motivated seller and a perfectly qualified buyer, but because of one mistake out of the starting line deal broke down.

The real mistake? Unclear thinking.

When selling a non-tech business, it’s priced based on a multiple of EBITDA. Inventory and accounts receivable? They’re part of what makes the business run, not separate add-ons. The investor gives you money to get money back. It’s really that simple.

If only someone had told the seller. Or John. Or both.

The Lesson: Businesses are sold off of EBITDA Multiples.

For those of you that might feel a little fuzzy on “EBITDA” - don’t feel bad, here’s a refresher:

Take the “Net Income” you see at the bottom of your P&L. Make sure it’s right.

“Add back” in 3 items - Interest you’ve paid to the bank, Tax Depreciation on Assets, and Tax Amortization on Intangible Assets.

That’s EBITDA

So if your net income last year were $1,250,000.00, but you had a small loan you paid $25,000.00 in interest on, $100,000.00 in Tax Depreciation, and then you were still paying down something like a non-compete from a previous owner to the tune of $75,000.00 a year, then your “EBITDA” would be $1,450,000.00 - a nice little bonus over your pure “Net Income” number.

The reason this metric is used is because, to a degree, EBITDA can be considered a better measure of the “true” earning potential of a business for the following reasons:

Interest is only incurred during the time period in which the loan persists. Once the loan goes away (gets paid off totally), the interest does too. So it isn’t as “permanent” as something like the Electric Bill, or Salaries, for example.

Tax Depreciation is known as a “non-cash” expense - no one actually comes and charges your bank account for the value of the Tax Depreciation on your Income Statement - it’s actually an “Accrual” adjustment that your tax preparer places on your books in an effort to simulate (within the laws of the tax code) how much money you’d need to spend, over time, to maintain the asset base of your business. This line item gets pretty complex sometimes as it applies to valuing companies, and it matters much, much more in asset heavy businesses like manufacturing compared to asset light businesses like Professional Services. Suffice to say, because this is considered an accounting “adjustment,” it gets added back on top of Net Income to try to get to a better approximation of the earning potential of a business.

Tax Amortization is in an identical position to Tax Depreciation, except with so-called “intangible assets,” which are assets like Intellectual Property that have been purchased from other companies, instead of physical assets like trucks, equipment, or buildings. It gets added back for the same reason that Tax Depreciation does - it’s an accounting “adjustment” to estimate what it might cost over a long period of time to maintain any Intangible Assets your company must own in order to maintain its business activity into the future.

Don’t get confused about the “Multiple” part in the EBITDA Multiples phrase either - it’s much easier to understand than EBITDA - It’s just how much to multiply the EBITDA number by to get to the final sale price.

An easy way to think about it is this: every “1” in the EBITDA multiple is equivalent to a year of running the company. So if you sell for a “4” EBITDA Multiple, what you’ve really done is receive 100% of all the earnings of the company for the next 4 years today, and the buyer then gets the opportunity to earn the next however many years the business is able to continue cashflowing on into the future.

So, EBITDA. And Multiples. And thus, EBITDA Multiples.

So far, so good.

It rarely stays good for long though, because it doesn’t take much time for most sellers to bring up a point that the vast majority find most salient:

“It’s all well and good to get paid for the EBITDA my company produces, that sounds just fine. But I of course also need to get paid for the stuff, you know, the assets I have in there. I know that I’m going to have to sell the equipment and the desks and things, but what about Inventory? And Accounts Receivable? I paid for all of that myself, if I leave it in there it feels like I’m not getting a fair deal.”

We hear this often. But here’s the truth.

Investors only really care about:

How much capital do I need to invest?

How much capital will I get back in return?

The assets you’ve invested in your business are only there to produce more cash flow.

This is why they look at EBITDA and why the EBITDA Multiple Method exists. It’s a proxy for cash flow and buyers want to now they’re getting a good ROI on their investment.

For example, if you had to pay 7x EBITDA for a business that wasn’t growing, the pretax return on the deal would be about 14% (See chart below). That means the after-tax return on that investment isn’t much better than putting money in the stock market and sitting on the beach. Buying a business is a whole lot more work & more risk.

And this explains exactly why you don’t typically mix an EBITDA valuation and asset valuation. It’s all about return on cash flow.

THAT’S A WRAP

Before you go: Here are 2 ways we can help

Is your deal stuck? We may be able to help. Get a free 30-minute deal assessment here — LINK TO SCHEDULE ASSESSMENT CALL

Are you an M&A Advisor or Broker looking for Wall Street-level financial analysis support for your CIMs and client financial info? If so, we offer a success fee-based program to help you close more deals with less overhead. To learn more, schedule a call here — LINK TO LEARN ABOUT SUCCESS-BASED FINANCIAL ANALYSIS

How did you like today's newsletter? |